When you begin looking for a therapist, one of the first decisions you need to make is what your budget looks like. Using your health insurance plan to pay for therapy can be confusing, but it's a good option for many folks because it can save you a lot of money.

This guide outlines all the ways insurance can be used to pay for therapy so you can learn how to maximize your plan and find a therapist who fits within your budget!

- Options for paying for therapy

- In-network vs. out-of-network therapists: What's the difference?

- In-network: How to pay for an in-network therapist

- Out-of-network: How to pay for an out-of-network therapist

- Insurance alternatives: Sliding scale, HSA, FSA

- Glossary and final thoughts

1. Options for paying for therapy

When it comes to paying for therapy, you have a few different options:

(a) In-network therapists

When you think of finding a therapist who "takes your insurance," you're thinking of in-network therapists. Finding an in-network therapist is generally the most affordable way to get therapy and are a good option if:

- You want to keep therapy costs under $50 per session

- Your copay is not affected by your deductible

- You've incurred a lot of medical costs this year

(b) Out-of-network therapists

Consider seeing an out-of-network therapist if:

- You're able to pay more than $50 per session and want to maximize your therapist options

- You have great out-of-network health insurance benefits

- You have to meet a high in-network deductible before your copay appliesYou're looking for a specialist, that is, a therapist who offers specializes therapies like EMDR

(c) Sliding scale, HSA, FSA

There are alternatives to health insurance too. This includes sliding scales and HSA and FSA plans. These are good options if:

- You have a high deductible plan and want to find alternative ways to keep therapy costs down

- You want to learn about financial need based flexible fees

- You're looking to use tax-free accounts through your employer

We'll look at each of these options in-depth in this article!

2. In-network vs. out-of-network therapists: What's the difference?

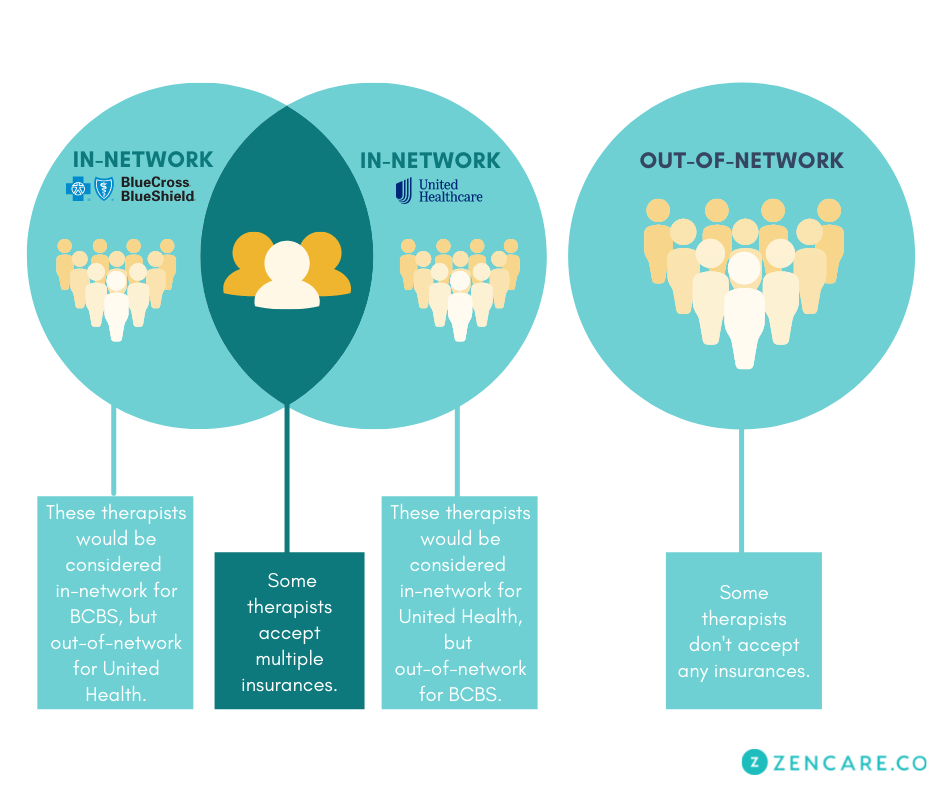

What does it mean to be in-network vs. out-of-network?

A therapist is in-network if they have a contract with your health insurance company to be part of their network of providers and accept a predetermined payment amount per session. You might also hear terms such as: take your insurance or accept your insurance.

A therapist is out-of-network if they don’t have a contract with your health insurance company and set their own fees. You might hear this referred to as: don't take or don't accept your insurance, accept PPO plans, or accept out-of-network benefits only.

Therapists decide which insurance networks they want to join and they do this for many different reasons. They can choose to accept some insurances but not others, only a few insurances, or none at all.

When looking for a therapist, deciding whether you are only looking for in-network therapists or if you are open to expanding your search to include out-of-network therapists is an important first step.

In-network therapists: Benefits and downsides

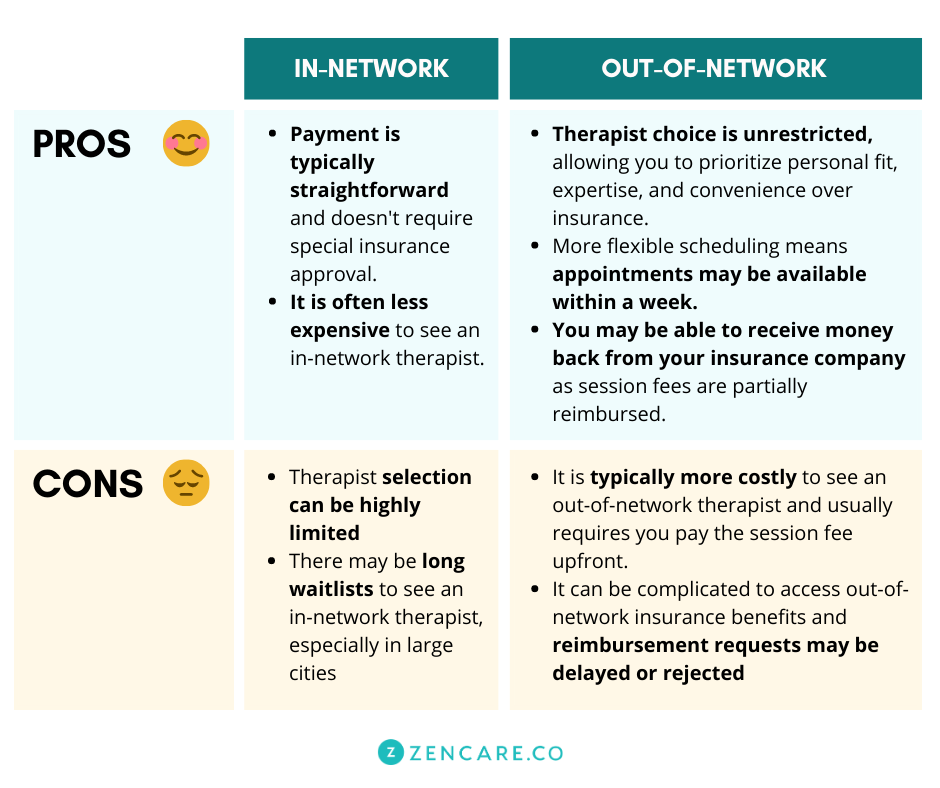

Benefits of seeing an in-network therapist include:

- Straightforward payment: Payment is typically straightforward and doesn't require special approval.

- Less expensive: It is often less expensive to see an in-network therapist because your health insurance plan pays the bulk of the session fee.

Downsides to limiting your therapy search to in-network therapists include:

- Limited therapist selection: Because of low payment and logistical hassle, many therapists choose not to be in-network with health insurances. This limits the pool of therapists from which you can choose a provider, which may mean that your chances of finding a therapist with a specific background, therapy modality, or personality decrease.

- Long waitlists: Because in-network therapists are so high in demand, good in-network therapists are often known in the community and fill up quickly. You may encounter long waitlists to see in-network therapists, especially in large cities.

Out-of-network therapists: Benefits and downsides

Including out-of-network therapists in your search will allow you to prioritize fit, expertise, and convenience, but often requires you to pay more for sessions and provide payment upfront.

Benefits of seeing an out-of-network therapist include:

- Greater pool of providers to choose from: When you expand your search beyond your health insurance network, your therapist choice is unrestricted, allowing you to prioritize personal fit, expertise, and convenience.

- Flexible scheduling: Out-of-network therapists may have greater availability, and more flexible scheduling means appointments can be available within a shorter time (i.e. one week).

- Potential for reimbursement: You may be able to receive money back from your health insurance company if your benefits include partial reimbursement for out-of-network mental health treatment.

Downsides to seeing an out-of-network therapist include:

- Higher costs: It is typically more costly to see an out-of-network therapist, and usually requires you to pay the session fee upfront. In cities like New York City and Boston, therapy sessions average $150 - $250 per session; in smaller cities like Providence, therapy sessions average $100 - $150 per session. You’ll have responsibility over a larger portion of this amount than if you saw an in-network therapist.

- Logistical hassle of out-of-network benefits: It can be complicated to access out-of-network insurance benefits and reimbursements requests may be delayed or rejected. Think: lots of paperwork! You can use a tool like Reimbursify to facilitate this electronically and receive the reimbursable amount via check.

Why therapists choose not to be in-network with health insurances

Therapists choose not to take insurance because they are paid less, have less time with clients, and lose autonomy over patient care and privacy.

Despite these issues, in-network therapists work with insurances to serve a diverse clientele, especially those who could not otherwise pay for a session. It is also easier to build a caseload as an in-network therapist because therapy seekers typically prioritize finding a therapist who takes their insurance.

By being out-of-network, therapists earn more, avoid the logistical hassles of insurance paperwork, and preserve more patient privacy.

3. In-network therapists: How to find and pay for an in-network therapist

How to find a therapist who takes your health insurance

You can find a therapist in-network with most insurances on Zencare.

Make sure to select your insurance company under "Insurances" to view therapists who are in-network with your insurance. You can also learn more about paying for therapy through the following health insurance companies:

Why aren't all insurances listed?

We are expanding our network of insurance-accepting providers, however, particularly in major cities, it can be difficult to find therapists who take insurances and are accepting new clients. Some insurance networks are also region-specific, an example being The Empire Plan network, which is only available in New York.

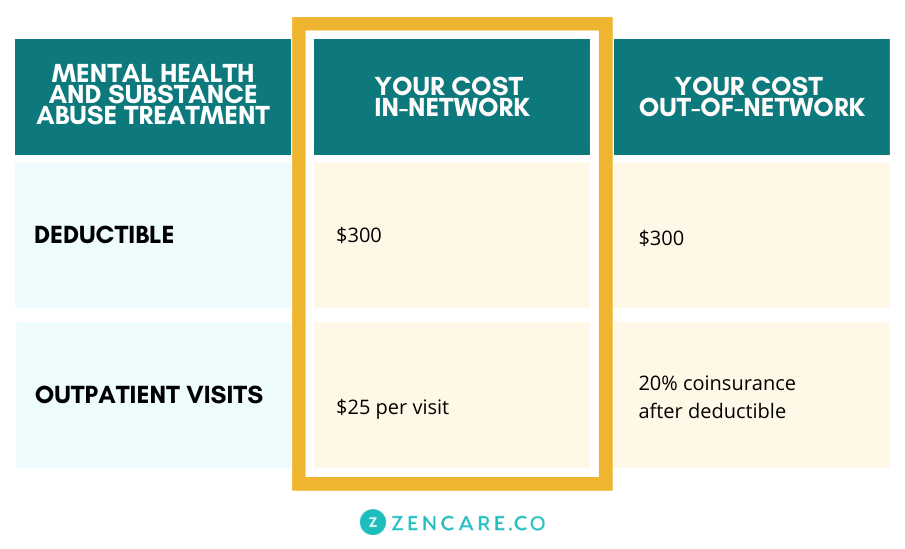

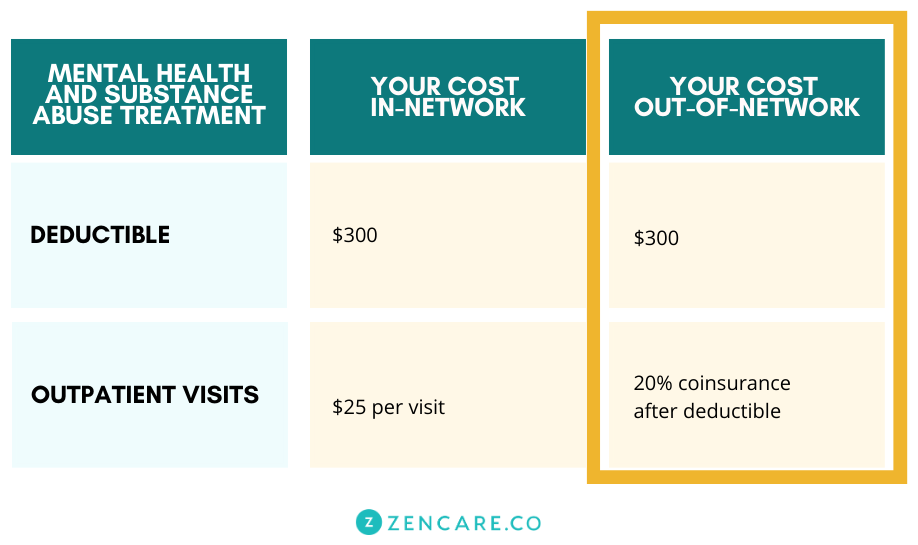

How payment for in-network therapy works

You can find complete information regarding your insurance coverage in your "Summary of Benefits." This chart is typically on your insurance company website or in a new member's packet:

There are two key terms that determine your payment amount:

- Deductible — The sum total of medical costs you need to pay each year before your insurance coverage begins.

- Copay — The set fee you pay at every therapy session.

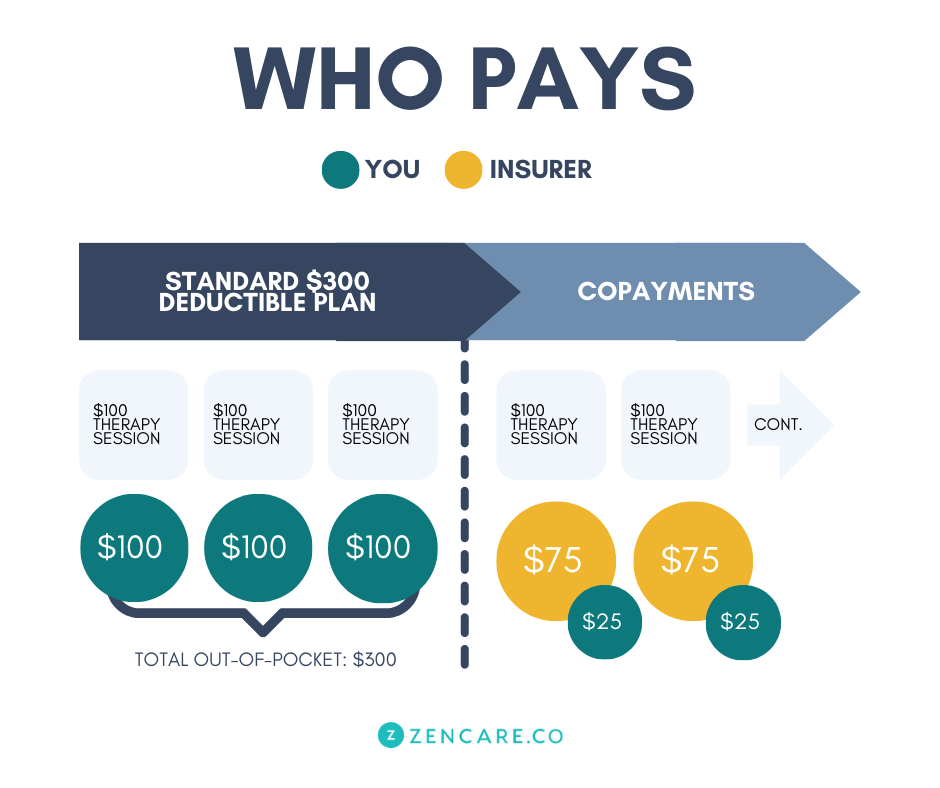

When you see a therapist who is in-network with your insurance plan, you pay them a copay at each therapy session. Then, your therapist sends a claim to the insurance company to receive the remainder of the fee they're owed.

In this example, the therapist's session fee is $100. You pay your therapist a $25 copay at each session and your therapist gets paid the remainder of the session fee ($75) by the insurance company:

Beware of the deductible!

While in-network payment may seem straightforward, you also need to consider your deductible to determine the total cost of a therapy session.

At each therapy session, you will either pay the therapist's full fee (typically the case if you are seeing an out-of-network provider) or your copay amount (this is typically the case if you are seeing an in-network provider). There are two possible scenarios in regards to what fees you can expect to pay at your session:

Scenario 1: You only pay your copayment fee before a therapy session. You do not need to meet your deductible, and so you would not need to pay the full session fee.

Scenario 2: Your insurance plan requires you to meet your in-network deductible before your copay applies. Meaning, you need to meet your deductible before you only pay your copay at your appointment. To meet your deductible, you could expect to pay your full session fee. You can also meet your deductible by paying for other medical expenses such as prescriptions or medical services — these will all contribute to meeting your deductible.

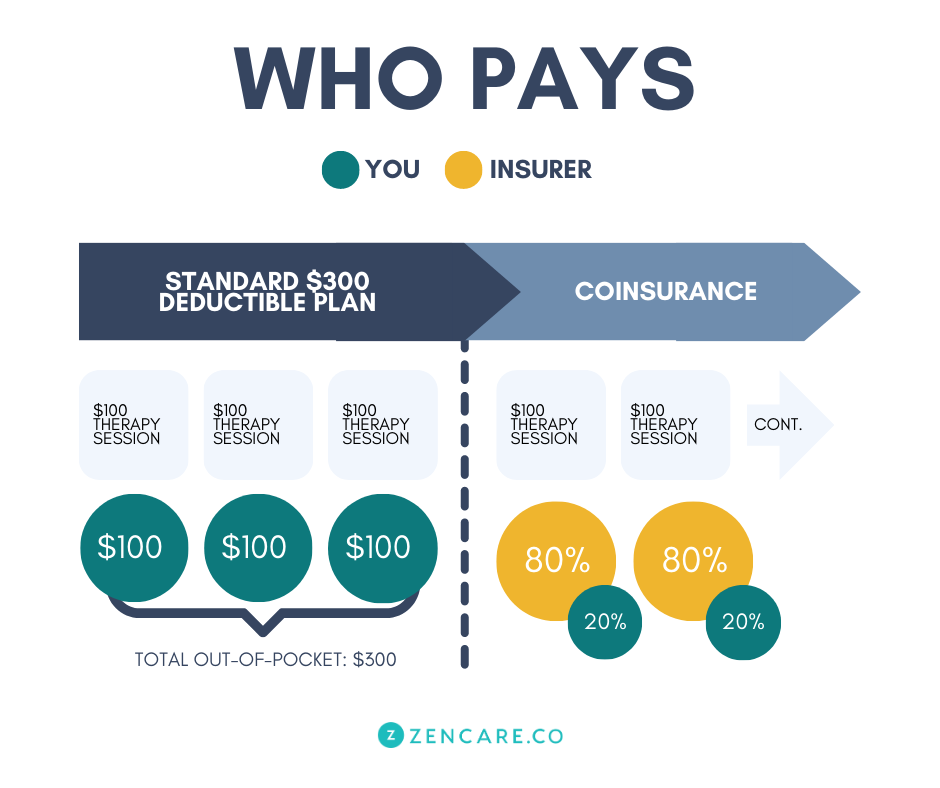

Let's say you haven't had any medical costs so far this year:

The therapist's session fee is $100, so you pay the full $100 fee for three sessions, at which point you've met your $300 deductible. At subsequent sessions, you pay only the $25 copay per session, and your insurance company pays the remaining $75 per session.

4. Finding and paying for an out-of-network therapist

Whenever possible, try not to limit your therapist search by insurance. By using out-of-network benefits, you can typically have a portion of each session fee reimbursed by your insurance company, making it more affordable to prioritize therapist fit and start therapy sooner.

Benefits of including out-of-network therapists in your search

There are many benefits to including out-of-network therapists in your therapist search.

Expanding your therapist search beyond insurance allows you to:

- Broaden your therapist pool: Especially for less common insurances or in major cities, it can be very, very difficult to find an in-network therapist. If the primary criteria of your search is insurance, you may immediately eliminate 99% of available therapists, leaving you with few options and little choice.

- Focus your therapist search on personality fit and expertise: Broadening your search beyond insurance gives you the opportunity to focus on other criteria, such as finding a therapist who is a true expert in a specific approach or mental health challenge. You can also focus on finding a therapist with whom you feel an immediate connection. The most important aspect of successful therapy is the therapist-client relationship, and when you have more choice, you are more likely to find someone just right for you.

- Decrease wait time to begin therapy: Since there is often great demand for therapists who are in-network with specific insurances, they frequently have long waitlists to accept new clients. Out-of-network therapists typically can accommodate new clients sooner and may be more flexible with your scheduling and clinical needs.

How payment for out-of-network therapy works

Let's return to the Summary of Benefits we saw before, and focus on out-of-network costs:

Now, we have a new term to introduce:

- Coinsurance — The percentage of a therapist's session fee you are responsible for paying.

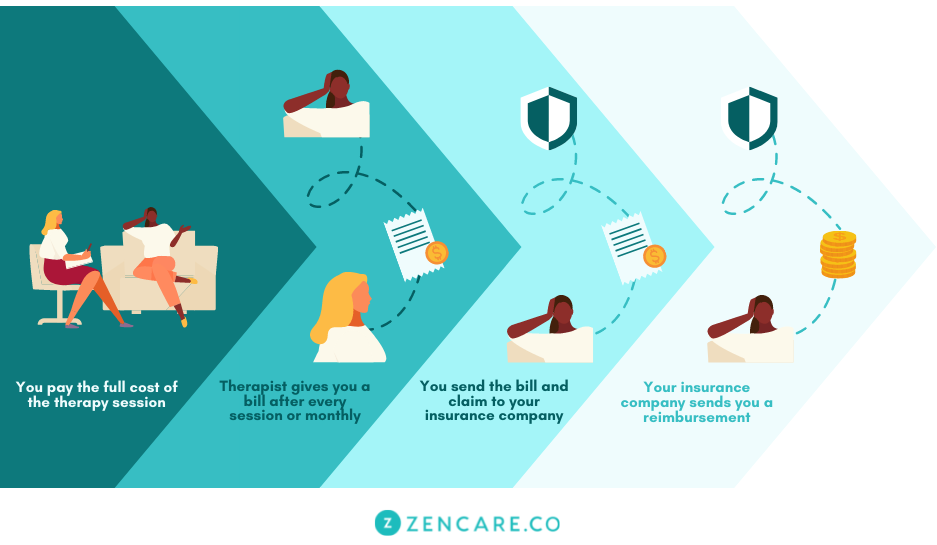

To use insurance benefits for sessions with an out-of-network therapist, you first pay the full session fee* at your therapy session. Afterwards, mail, fax, or submit a claim online to the insurance company, and receive reimbursement in the form of a check. The claim may be submitted after every session, or in aggregate every month.

As a result of the reimbursement from your insurance company, you ultimately pay only a set percentage of the therapist's fee; in this example, 20% of the session fee.

*Therapy session fees typically range between $80 - $150 in smaller cities and $100 - $250 in big cities; session fees are typically higher for psychiatrists.

Note that in this example there is still a $300 deductible, so you may not receive insurance reimbursements until you've paid $300 in total medical costs.

Beware of the allowable amount!

The actual amount you are reimbursed by your insurance company is not based on what the therapist charges per session; rather, reimbursement is based on a predetermined amount that the insurance company sets.

- Allowable amount (or "usual, customary, and reasonable rate") — The fee an insurance company determines is reasonable for a therapist to charge per session.

The allowable amount varies by geography and therapist degree type. Unfortunately, insurance companies do not disclose this amount so you won't know exactly how much of your session will be covered until you submit your first claim and receive reimbursement.

In this example, the therapist's fee is $100, so you pay $100 per session upfront. However, let's say the insurance company sets the allowable amount at $80 per session.

This means that the insurance company will reimburse you at a rate of 80% of $80. You will ultimately be responsible for 20% of $80, plus 100% of the remainder of the actual cost of therapy ($20).

The math behind the "allowable amount"

Let's break down the math behind the allowable amount to determine your total cost for ongoing therapy sessions, after meeting your deductible:

- Therapist's session fee = $100

- Allowable amount = $80

- Coinsurance = 20% (Insurance pays 80%)

This means:

- You pay $100 upfront and submit a bill for the session to your insurance company.

- The insurance company reimburses you for 80% of the allowable amount:

80% x 80 = $64

You are reimbursed $64. - You have paid:

Coinsurance (20%) x Allowable amount (80) = $16

Plus the difference between Session Fee ($100) - Allowable amount ($80) = $20

$16 + $20 = $36

= Your total payment is $36.

How to find out your out-of-network benefits

The best way to fully understand your out-of-network coverage is to call your insurance company. The number for member services is typically on the back of your insurance card.

When you call your insurance company, be sure to ask:

- What is my annual deductible?

- Do I have an additional out-of-network deductible?

- What is my coinsurance for outpatient mental health?

- Do I need a referral from a primary care physician or an in-network therapist to see an out-of-network therapist?

- How do I submit out-of-network claims for reimbursement?

Beware of high deductible plans

Recall: a deductible is the total cost you need to pay before your insurance coverage begins.

So far, we've looked at how payment works to see an in- and out-of-network therapist when the deductible is set at $300.

Unfortunately, a deductible can be much higher. A high deductible heavily influences how much you pay for therapy.

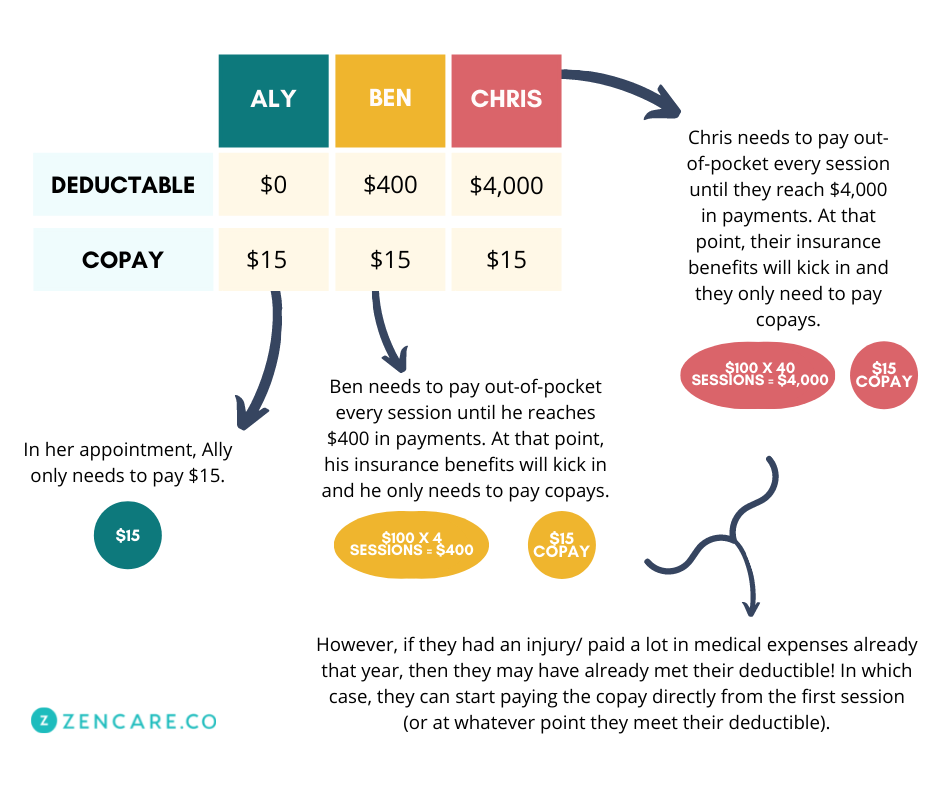

For example, let's say the three people below are all seeing the same therapist in-network with the same insurance company, but different deductible plans where they must meet their deductible before their copay applies:

Ally pays only $15/session.

Ben pays the full session fee of $100/session for 4 sessions to meet his $400 deductible, and then pays $15/session.

Chris pays the full session fee of $100/session for 40 sessions to meet his $4,000 deductible, and then pays $15/session.

Let's look at some options to make therapy more affordable when you have a high deductible health insurance plan.

5. Insurance alternatives: Sliding scale, HSA, FSA

If you're struggling to find available in-network therapists, can't afford average out-of-network therapist session fees, and/or have a high deductible plan, there are still ways to afford therapy.

Option 1: Sliding scales

A sliding scale represents the range of fees a therapist typically charges per session.

For example, while a therapist's standard fee may be $150 per session, they might list a sliding scale of $80 - $150 per session. This means that they are willing to work flexibly within your budget and offer lower fees based on financial need. If you can only afford $100 per session, they might be willing to work with you at that amount.

Therapists typically list a lower limit in order to ensure they earn a livable annual salary. Likewise, while they may reserve a few sliding scale slots for clients who would not otherwise be able to seek therapy, these slots are typically limited; not all clients can pay the lowest limit fee at any given time.

You might ask about sliding scales on your initial call with a therapist if you know you have a high deductible. Just be aware that your request may be declined, depending on how many clients a therapist already has paying low fees.

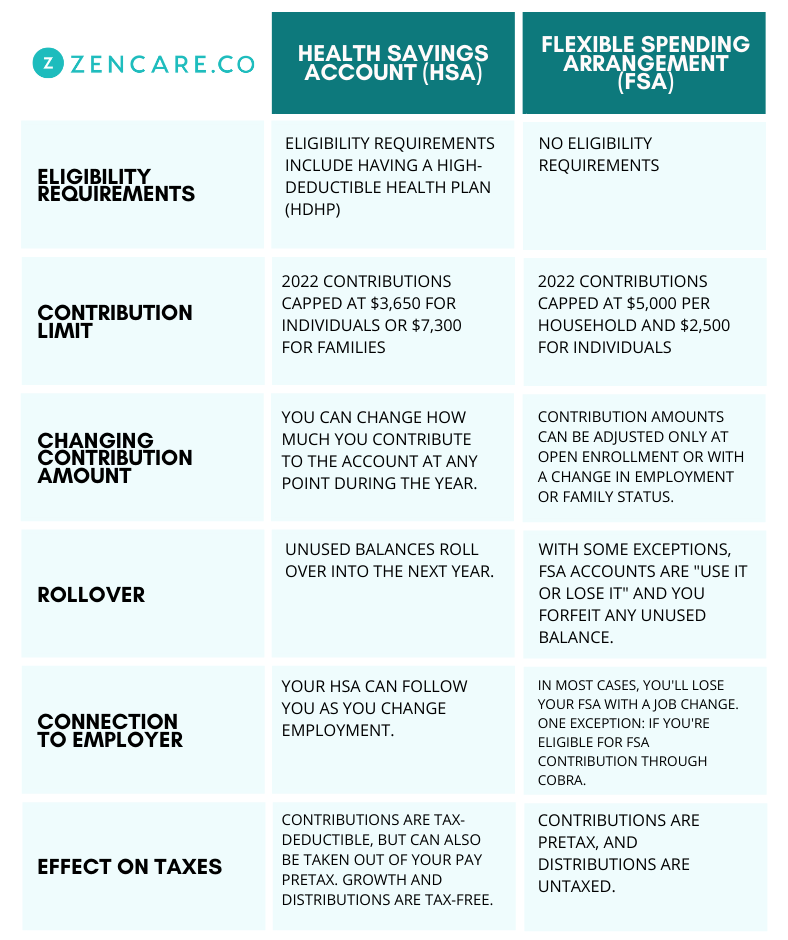

Option 2: HSAs and FSAs

Health Savings Accounts (HSAs) and Flexible Spending Accounts (FSAs) are two ways employees can pay for health-related expenses, including copayments and coinsurances, through a tax-free account.

HSA and FSAs allow you to set aside funds for medical expenses while reducing your taxable income. In most cases, you receive a debit card for your account and use it to pay for qualifying expenses throughout the year. While you can’t enroll in both types of accounts, employers may offer the choice of both options.

HSAs allow you to contribute up to $3,450 per year, roll over unused balances to the next year, and transfer balances as you change employment; however, there are eligibility requirements, such as having to be enrolled in a high-deductible health plan.

FSAs don't have eligibility requirements; however, they are capped at $2,650 and you forfeit any unused balances in a given year.

This great chart from Nerdwallet outlines the major differences between HSAs and FSAs:

6. Glossary & Final Thoughts

Phew! That was a lot of ground to cover.

If your brain isn't bursting yet, below are definitions for some other terms you may come across in your insurance journey.

Insurance plans terms

- HMO: An insurance plan that typically has lower monthly premiums but less flexibility in out-of-network coverage. If you have this kind of plan, your options may be limited in-network, but it could be much more expensive to see an out-of-network therapist. You are also typically required to see a primary care physician for a referral to therapy before your insurance company will provide coverage.

- PPO: An insurance plan that may have higher monthly premiums, but more flexibility in out-of-network coverage. If you have this kind of plan, your costs to see an in- or out-of-network therapist may be comparable.

- EPO: An insurance plan with a similar benefit structure to an HMO, but you usually don't need to see a primary care physician for a referral before accessing mental health services.

- POS: An insurance plan where, like an HMO, you need to see a primary care physician for a referral to therapy, but once you receive the referral, you will receive better out-of-network coverage. Similarly to a PPO, your cost to see a therapist in- or out-of-network may be comparable.

Payment-related terms

- Claim: A bill you or a therapist supplies to the insurance company in order to seek reimbursement.

- Out-of-pocket: Your own money; paid by you, rather than an insurance company.

- Out-of-pocket limit: The maximum amount of your own money you can pay in one year for deductibles, copays, and coinsurances; if you reach this amount, your insurance company subsequently provides 100% coverage.

- Premium: The amount you need to pay every month for insurance coverage.

Therapy-specific terms

- Billing code: A 5-digit number that tells an insurance company what kind of services were provided in a given session so they know how much to reimburse you or your therapist. On an initial call, it's a good idea to ask your therapist what billing codes they use if you're seeking out-of-network coverage. Then, you can call and ask your insurance company how much you'll be reimbursed for those specific services.

- Cancellation fee: The amount you need to pay a therapist if you cancel a session on short notice. Insurance companies don't pay for sessions that don't occur, so you are typically responsible for the therapist's full session fee. Make sure you go over and understand your therapist's cancellation policy at the first session!

- Diagnostic code: A 4-digit number used to signify a diagnosis. Therapists are required to assign you a diagnostic code if you are using insurance benefits to pay for therapy. This shows the insurance company that there is a medically valid reason for the session to have occurred, and therefore the therapist deserves to be paid.

- Outpatient mental health: The term used for a therapy session in an insurance summary & benefits.

Now my brain is bursting. What should I do?

That's completely understandable — navigating health insurance is complicated!

First, know that you're not alone. Even our team members at Zencare get confused when using our own health insurance plans for therapy!

Second, choose the route that feels most manageable for you right now, whether this means finding an in-network therapist, finding an out-of-network therapist, or finding therapists who offer alternatives like a sliding scale.

Third, speak with your therapist. After seeing hundreds of clients, therapists are well-versed in how insurances work. They may not have all the answers, but can help guide you in the best next step. If you're in college, you might also try asking Counseling Services for guidance.

Finally, even though it's everyone's least favorite option, calling your insurance company often clears up a lot of confusion, once you get a human on the line. To make it less daunting, consider preparing a list of questions ahead of time. You've got this!