Clinically reviewed by Natalie Asalgado, LCSW. Published on January 16, 2025.

The new year is a great time to reassess your health priorities and set yourself up for success, especially when it comes to your mental health. Therapy can be life-changing, but many people leave valuable health insurance benefits on the table simply because they don’t know how to maximize them. Understanding how to use your health insurance policy efficiently can significantly lower your out-of-pocket expenses, reduce stress, and help you begin accessing therapy benefits right away.

Navigating the healthcare system can feel overwhelming, but it doesn’t have to be. In this guide, we’ll walk you through strategies to make the most of your insurance plans, and how to start using your benefits for therapy early in the year. By following these steps, you’ll save on healthcare costs in the long run and enjoy the peace of mind that comes with prioritizing your mental well-being.

Understand Your Health Insurance Policy

The first step to making the most of your insurance is understanding your health insurance policy. Every plan is different, so it’s essential to review your summary of benefits to identify what’s covered and how to access those benefits.

Key areas to focus on include:

- Mental health services: Confirm whether therapy and other related healthcare services are covered. Many plans include coverage for in-person therapy sessions, teletherapy, and even wellness programs.

- In-network providers: Using healthcare providers within your plan’s network is a great way to lower costs. Out-of-network therapists could result in higher out-of-pocket costs and may not count toward your annual in-network deductible or in-network out-of-pocket maximum.

Your insurance plan should come with a Summary of Benefits Coverage guide. This outlines exactly what your specific plan covers from physical health to mental health. There is typically a section called, “Mental Health Services” where benefits like inpatient visits or outpatient group/individual therapy visits are listed along with what your insurance coverage is.

Your insurance company or provider is a valuable resource for clarifying any details about your insurance plans. Don’t hesitate to contact them for help understanding your benefits or finding the right health care providers.

Leverage Your Health Insurance Plan’s Benefits Early

Timing is crucial when it comes to maximizing your insurance benefits. Many health insurance policies reset at the start of the new year, meaning your annual deductible begins again. Meeting your deductible early can significantly reduce out-of-pocket expenses for the rest of the year.

Here’s how to get started:

- Schedule therapy early: Booking therapy sessions at the beginning of the year is a great way to ensure consistent care while working toward your deductible. This strategy helps you take full advantage of the benefits your plan offers.

- Address chronic conditions: If you’re managing long-term mental health challenges, like anxiety or depression, now is the time to prioritize consistent therapy and related health care services.

- Utilize preventive care: Use the preventative care benefits included in your plan to schedule mental health assessments or therapy consultations early.

By starting early, you’re setting yourself up for a healthier year and making the most of your insurance benefits.

Maximize Savings with FSAs and HSAs

One of the most effective tools for managing healthcare expenses is taking advantage of a Flexible Spending Account (FSA) or a Health Savings Account (HSA). These accounts allow you to set aside pre-tax dollars to cover qualified medical expenses, including therapy, prescription drugs, and other mental health-related costs.

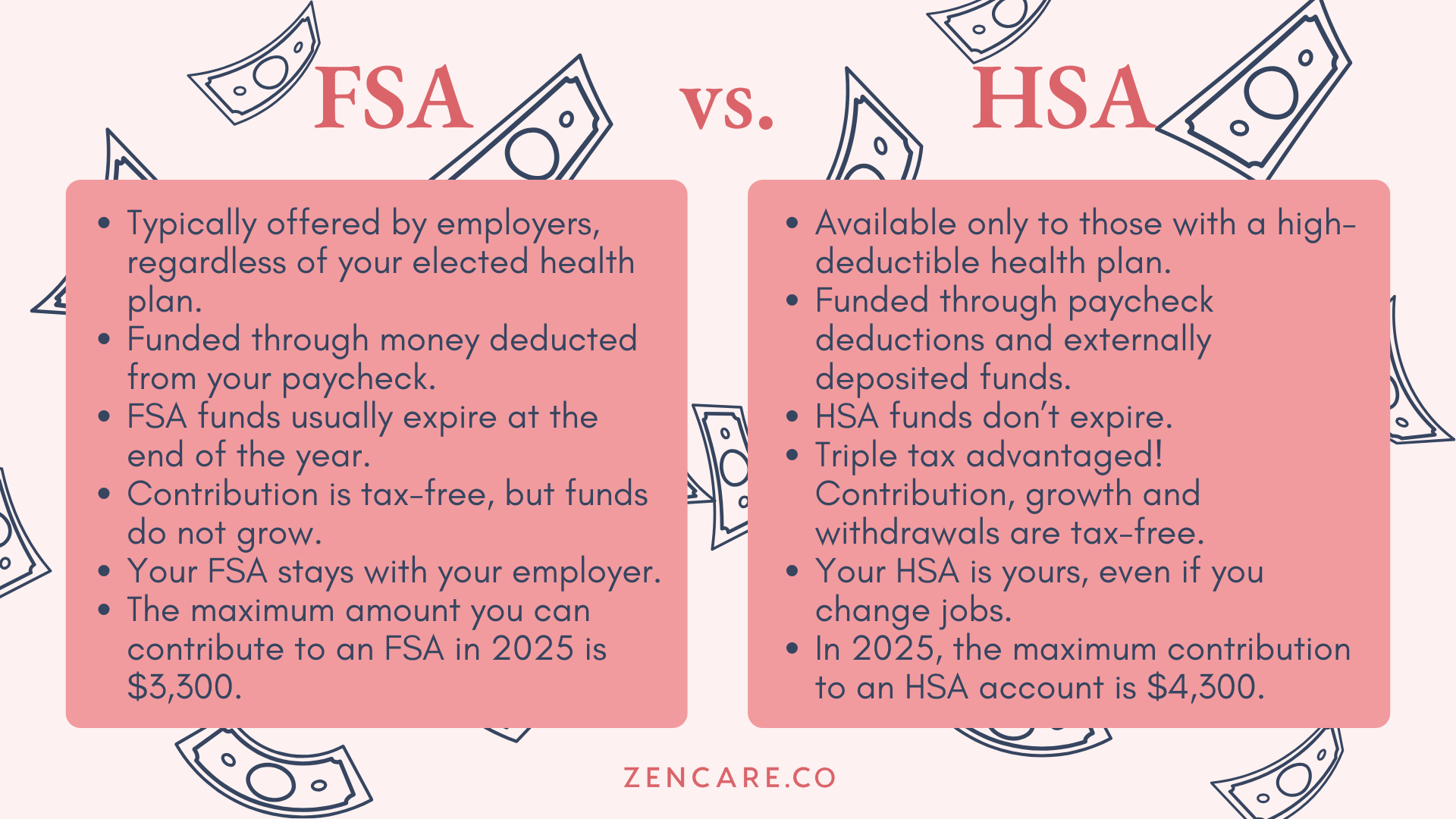

- FSAs: Typically offered by employers, a Flexible Spending Account (FSA) lets you use pre-tax dollars to pay for out-of-pocket healthcare costs. You elect an amount you want deducted from your paycheck each pay period to go into your FSA. Remember, FSA funds usually expire at the end of the year, so it’s important to plan accordingly. The maximum amount you can contribute to an FSA in 2025 is $3,300. Your funds are typically available as early as January 1.

- HSAs: Available to those with a high-deductible health plan, HSAs allow you to save money for medical expenses. You can contribute to your HSA through paycheck deductions like an FSA, but you can also directly deposit funds into this account from another bank account, for example. Contributions roll over year-to-year, making it a valuable resource for long-term savings. In 2025, the maximum contribution to an HSA account is $4,300 if you are covered by a high-deductible health plan just for yourself, or $8,550 if you have coverage for your family.

Both accounts can be used for therapy, prescription medications, and any other qualifying medical expense.

Choose In-Network Providers for Lower Costs

Using in-network providers is one of the simplest ways to reduce your healthcare costs. These providers have pre-negotiated rates with your insurance company, ensuring you pay less for therapy and other medical services.

- Benefits of staying in-network:

- Lower out-of-pocket maximum and additional cost savings.

- Easier to meet your annual deductible.

- Fewer surprises when it comes to medical bills.

On Zencare, to find therapists who are in-network with your insurance, use the Insurance filter and select your insurance plan from the drop down. This will help you narrow your choice of therapists to ones you know take your insurance.

Some people prefer a therapist who is out-of-network due to their specific qualifications, location or existing relationship, for example. If this sounds like you, check with your insurer about partial reimbursement options. However, remember that this may increase your out-of-pocket costs — so make sure that you are able to pay the full amount for your sessions up front, even if you expect reimbursement.

Using Out-of-Network Benefits

While staying within your plan’s network is often the most cost-effective option, many health insurance plans also include out-of-network benefits. These benefits allow you to work with therapists who may not directly partner with your insurance company but still offer partial reimbursement for your sessions.

What Are Out-of-Network Benefits?

- Out-of-network benefits provide partial coverage for care received outside your plan’s network.

- You’ll typically need to pay upfront for therapy sessions and submit claims to your insurer for reimbursement.

- Coverage varies but may include a percentage of the cost after meeting your annual deductible or out-of-pocket maximum.

Which Plans Include Out-of-Network Benefits?

- PPO Plans: Preferred Provider Organization (PPO) plans generally have robust out-of-network benefits, making them a good choice if you prefer flexibility in choosing healthcare providers.

- POS Plans: Point of Service (POS) plans may offer some out-of-network benefits, but typically require a referral from your primary care doctor.

- High-Deductible Health Plans (HDHPs): High-deductible health plans may include out-of-network coverage, but you’ll often need to meet a high deductible first.

How to Maximize Out-of-Network Benefits:

- Verify your health insurance coverage to confirm the reimbursement rate for out-of-network care.

- Ask your therapist if they can provide a “superbill,” a detailed receipt required by insurers for claims. You can also ask for the CPT (Current Procedural Terminology) codes ahead of time to get a more accurate quote for the reimbursement rate.

- If you are facing financial hardships, consider negotiating a sliding scale fee with your therapist to reduce upfront out-of-pocket costs.

While using out-of-network benefits may involve more effort, it’s a great way to access specialized care or maintain continuity with a therapist you trust.

Combine Therapy with Preventive Services

Many health insurance plans encourage the use of preventive services to address healthcare needs before they become larger issues. Combining therapy with other forms of preventive care is a great way to holistically manage your mental health.

Examples of preventive services include:

- Annual check-ups with your primary care provider or primary care doctor.

- Flu shots to maintain physical health alongside mental wellness.

- Mental health screenings to catch early signs of anxiety, depression, or other conditions.

Preventive care not only supports your good health but also ensures you’re using your health insurance coverage to its fullest potential.

Plan for the End of the Year

As the current year progresses, keep an eye on your healthcare spending to ensure you’re maximizing your benefits. Many insurance plans include resources like wellness incentives or coverage for elective medical procedures that may expire if unused. Take note if you hit your deductible, and what that could mean for the medical expenses you have for the rest of the year.

Here’s how to stay on top of your benefits:

- Track healthcare expenses: Keeping a record of therapy sessions and other costs can help you prepare for future needs and avoid unexpected bills. If your insurance company has an app — keep it downloaded and check in on your deductible, out-of-pocket maximums, and claims easily.

- Use FSA funds before they expire: If you have an FSA, make sure to use those funds for therapy or other health-related medical services before the end of the year.

- Plan ahead for next year: Consider how your needs may change and adjust your coverage during the open enrollment period to ensure you’re set up for success.

Additional Tips for Maximizing Your Insurance

- Build a relationship with your primary care provider: They can help coordinate care, refer you to in-network therapists, and ensure your mental health is a priority.

- Explore wellness programs: Some insurance providers offer programs focused on mental health or stress management, which can complement therapy.

- Ask about additional benefits: Check with your insurer to see if they cover teletherapy, group therapy, or other nontraditional forms of care.

- Budget for elective care: If you’re considering elective procedures like neuropsychological testing or mindfulness programs, verify coverage and costs upfront.

The Long-Term Value of Mental Health Care

Investing in your mental health pays off in the long run. By using your health insurance benefits effectively, you can reduce the overall cost of health insurance while ensuring access to essential services like therapy, prescription drugs, and preventive care.

Maximizing your benefits also helps you avoid the financial stress of unexpected bills, giving you the peace of mind to focus on what matters most — your well-being.

Feel Empowered by Your Insurance Plan

The new year is the perfect time to start maximizing your health insurance benefits for therapy. By understanding your health insurance policy, leveraging preventive care, and staying within your plan’s network, you can reduce out-of-pocket expenses and begin therapy with confidence.

Ready to take the first step? Platforms like Zencare are a valuable resource for finding providers who meet your needs. Don’t wait — take advantage of your health insurance coverage today to prioritize your mental health and set the tone for a healthier, happier year ahead.